Welcome to the Fitob R Package

The main focus of the Fitob R Package is the PDE-based financial derivative pricing.

Fitob is able to solve not just the Black-Scholes PDE in a multi-dimensional setting,

but also the more general Fokker-Planck (convection-diffusion) PDE.

Fitob provides a general scripting interface that can describe almost any financial

contract in an efficient and unique way. This feature is demonstrated by several examples.

Important links:

- Manual and Tutorial of the Fitob R Package here

- Download Fitob R Package here

- The project summary page you can find here

The following examples illustrate the PDE-based pricing approach of financial contracts (you can find more examples

with detailed explanations in the examples section of the

manual ):

-

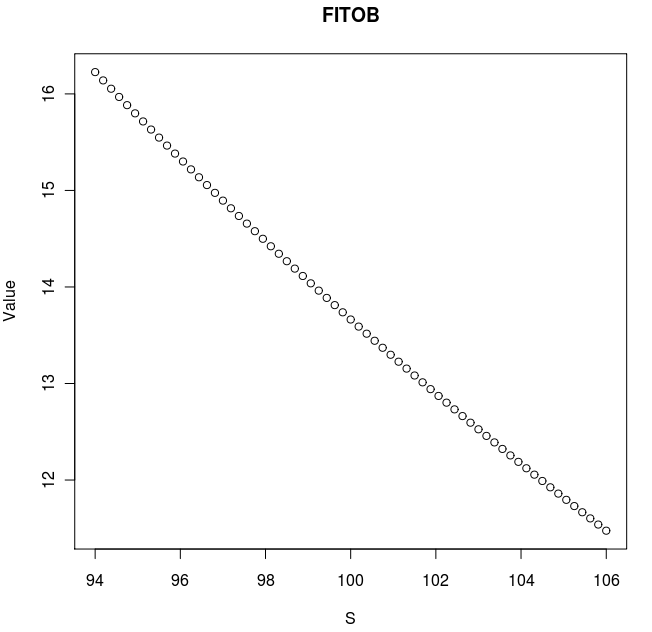

Pricing a 1D American Option. The plot shows the resulting price curve.

You can download the necessary files under:

american1D.xml ,

american1DScript .

In order to run the example, install Fitob and type in R (assuming that american1D.xml and american1DScript are in the current directory):

> require(fitob);

> liMy = fitobPriceMesh("american1D.xml" , "american1DScript",5);

> fitobMeshPlot(liMy);

> liMy[[1]] #the scalar price

-

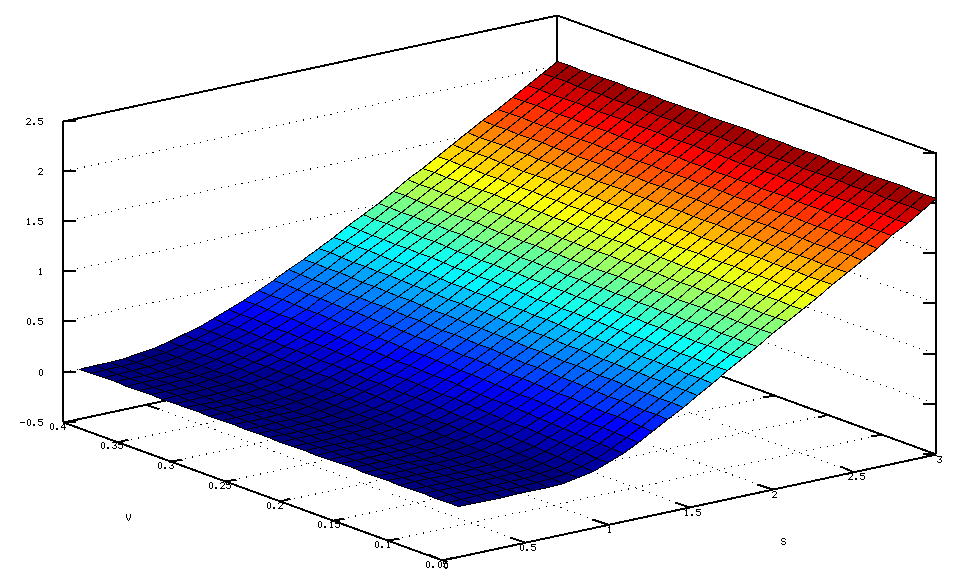

Pricing a 1D Option under the Heston process. The plot shows the resulting price surface in 2D.

You can download the necessary files under:

Heston2D.xml ,

Heston2D_Script .

In order to run the example, install Fitob and type in R (assuming that Heston2D.xml and Heston2D_Script are in the current directory):

> require(fitob);

> liMy = fitobPriceMesh("Heston2D.xml" , "Heston2D_Script",5);

> fitobMeshPlot(liMy);

> liMy[[1]] #the scalar price

-

Early withdrawal boundary for a Guaranteed Minimum Withdrawal Benefit (GMWB) modelled in 5D.

A is the account of the benefit, S is the underlying's price. (see J.Benk, D. Plueger: Hybrid Parallel Solutions of the Black-Scholes PDE with the Truncated Combination Technique. In Proceedings of the HPCS conference, 2012 Madrid.)

- If you want to price your own financial contract, it is recommended to take one example

( from here )

and modify it incrementally.

If you face any problems please do not hesitate to write to (benkjanos at gmail dot com)